India’s Goods and Services Tax (GST) framework is undergoing its most significant transformation since its inception in 2017. Prime Minister Narendra Modi’s announcement of GST 2.0 during Independence Day 2025 has set the stage for sweeping reforms that promise to simplify taxation, reduce compliance burden, and deliver substantial benefits to consumers and businesses alike. These changes represent a paradigm shift towards a more streamlined, secure, and efficient tax system that addresses the longstanding challenges faced by taxpayers across the country.

The Revolutionary GST 2.0: Moving Towards Simplification

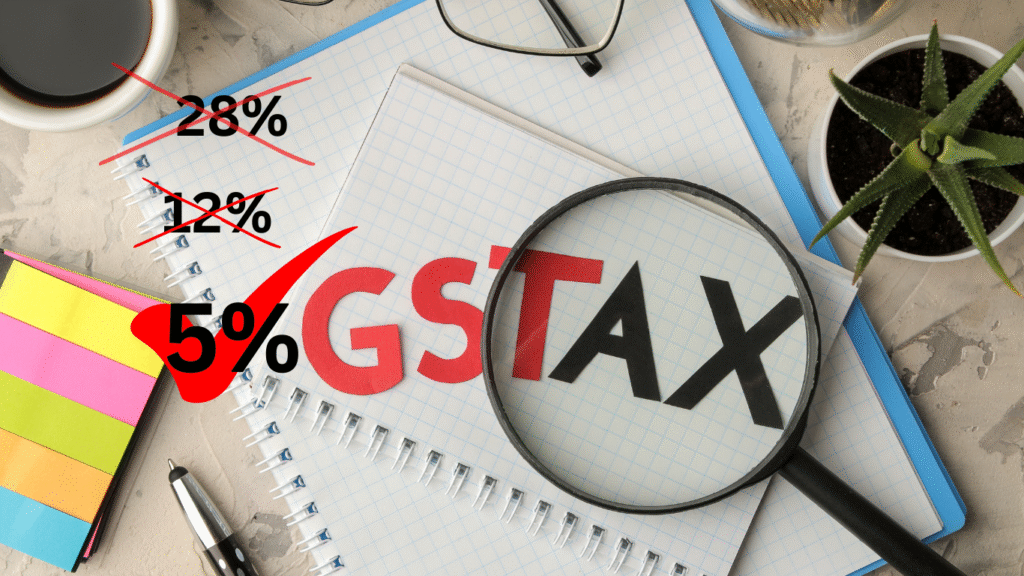

The centerpiece of India’s GST reform agenda is the proposed two-slab structure that will fundamentally reshape the indirect tax landscape. The current complex four-tier system comprising 5%, 12%, 18%, and 28% rates will be consolidated into just two main slabs of 5% and 18%, along with a special 40% rate for luxury and sin goods.

This transformation is expected to benefit consumers significantly, with 99% of items currently in the 12% bracket moving to 5% and approximately 90% of goods and services from the 28% slab shifting to 18%. The finance ministry has emphasized that this restructuring will focus on three core pillars: structural reforms, rate rationalization, and ease of living.

The Group of Ministers (GoM) on GST rate rationalization has already accepted the Centre’s proposal, paving the way for implementation by Diwali 2025. This timing is strategic, as PM Modi announced it as a “double Diwali gift” to the nation, coinciding with the festive season when consumer spending typically peaks.

Expected Consumer Benefits

The proposed rate restructuring will deliver tangible benefits across multiple sectors. Air conditioners, televisions, and personal care products are expected to become more affordable under the new structure. Small cars and SUVs will see their GST rates reduced from the current 28% plus cess to 18%, potentially resulting in savings of ₹50,000 on a ₹5 lakh vehicle. Similarly, motorcycles below 350cc, footwear below ₹1000, and clothes above ₹1000 will benefit from reduced taxation.

The hospitality sector will also see significant changes, with business class travel and hotels below ₹7,000 per night moving from 12% to 5% GST. Health and life insurance premiums may attract only 5% GST or become completely exempt, providing relief to policyholders.

Strengthening Digital Security and Compliance

Multi-Factor Authentication (MFA) Implementation

One of the most significant compliance changes is the mandatory implementation of Multi-Factor Authentication (MFA) for all GST taxpayers. This security enhancement follows a phased approach:

- January 1, 2025: Mandatory for taxpayers with Annual Aggregate Turnover (AATO) exceeding ₹20 crore

- February 1, 2025: Extended to taxpayers with AATO exceeding ₹5 crore

- April 1, 2025: Enforced for all taxpayers regardless of turnover

The MFA system requires users to authenticate using username, password, and OTP sent to registered mobile numbers, significantly enhancing portal security and reducing fraudulent activities. This measure builds upon existing requirements that have been mandatory for businesses with turnover exceeding ₹100 crore since August 2023.

E-Invoicing Threshold Reduction

The government has lowered the e-invoicing threshold to ₹10 crore effective April 1, 2025. This change brings many small and medium enterprises into the e-invoicing framework, requiring them to upload invoices to the Invoice Registration Portal (IRP) within 30 days of issuance. Non-compliance with this requirement will result in the loss of Input Tax Credit (ITC), making timely reporting critical for businesses.

Enhanced E-Way Bill Regulations

Starting January 1, 2025, e-Way Bill generation will be restricted to base documents not older than 180 days. This measure aims to prevent backdating of invoices and curb fraudulent practices. Additionally, Two-Factor Authentication (2FA) becomes mandatory for e-Way Bill generation, further strengthening the system’s security.

Mandatory Input Service Distributor (ISD) Registration

A crucial change effective April 1, 2025, is the mandatory ISD registration for businesses with multiple GST registrations under the same PAN. Previously, businesses could choose between the ISD mechanism and cross-charge method for distributing common input services. The new regulation requires:

- Obtaining separate ISD registration despite having regular GST registration

- Filing monthly GSTR-6 returns for ITC distribution

- Proper bifurcation of expenses between ISD and cross-charge transactions

- Updated vendor communication with ISD GSTIN details

This change aims to enhance transparency in ITC allocation and prevent accumulation at single locations.

GST Amnesty Scheme 2025: Relief for Taxpayers

The GST Amnesty Scheme under Section 128A provides significant relief to taxpayers with outstanding disputes from July 1, 2017, to March 31, 2020. Key features include:

- Complete waiver of interest and penalties on payment of principal tax amount

- Payment deadline: March 31, 2025

- Application deadline: June 30, 2025

- Mandatory appeal withdrawal for scheme eligibility

The GSTN has introduced a practical feature allowing taxpayers to submit screenshots of appeal withdrawal applications, enabling scheme participation without waiting for official court confirmations.

Sectoral Reforms and Specific Changes

Hospitality Industry Transformation

The hotel industry undergoes significant reform with the abolition of the “Declared Tariff” concept. GST will now be levied on actual transaction values rather than pre-declared tariffs. Hotels charging more than ₹7,500 per day will attract 18% GST with full Input Tax Credit availability.

Used Car Market Rationalization

A uniform 18% GST rate now applies to the margin value for all categories of used cars, regardless of engine size or fuel type. This harmonization eliminates previous rate differentiation and simplifies compliance for dealers in second-hand vehicles.

Invoice Series and Documentation Updates

Businesses must implement new sequential invoice series from April 1, 2025, ensuring unique, year-specific numbering. The IRN generation system will follow case-insensitive formatting from June 1, 2025, treating invoice numbers like ABC101, abc101, and Abc101 as identical and auto-converting to uppercase.

Composition Scheme Enhancements

The GST Composition Scheme continues to provide simplified compliance for small businesses in 2025. Current eligibility criteria include:

- Manufacturers and traders: Annual turnover up to ₹1.5 crore

- Special category states: ₹75 lakh turnover limit

- Service providers: Annual turnover up to ₫50 lakh

Tax rates remain attractive at 1% for manufacturers and traders (0.5% CGST + 0.5% SGST) and 6% for other service providers (3% CGST + 3% SGST). The opt-in period for FY 2025-26 was February 4 to March 31, 2025.

Reverse Charge Mechanism (RCM) Updates

The Reverse Charge Mechanism has seen important updates, particularly regarding commercial property rentals. The 54th GST Council meeting recommended bringing rental of commercial property by unregistered persons to registered persons under RCM to prevent revenue leakage.

Key RCM compliance requirements include:

- Monthly payment by 20th of the following month

- Separate record maintenance for RCM supplies

- ITC availability subject to eligibility conditions

- Self-invoicing for purchases from unregistered suppliers

Recent clarifications specify that for unregistered supplier RCM transactions, the financial year for ITC limits should be when the recipient issues the invoice.

Economic Impact and Revenue Implications

According to S&P Global Ratings, the proposed two-tier GST structure could reduce the effective taxation rate while boosting long-term fiscal revenues. SBI Research estimates that the combined impact of GST reforms and recent income tax changes amounts to approximately 1.6% of GDP in additional consumption expenditure.

The government currently derives 65% of GST revenue from the 18% slab, making it the largest contributor. The 28% slab contributes 11%, while the 12% and 5% slabs provide 5% and 7% respectively. By consolidating slabs, the government aims to simplify taxation and reduce compliance issues while maintaining revenue neutrality.

Implementation Timeline and Preparatory Steps

The implementation follows a carefully planned timeline:

January 2025: MFA for high-turnover businesses and e-Way Bill restrictions commence

February 2025: MFA expansion to mid-tier businesses

April 2025: Universal MFA implementation, ISD registration mandate, and e-invoicing threshold reduction

June 2025: Case-insensitive IRN generation begins

October 2025: GST 2.0 rate structure implementation by Diwali

Businesses must undertake several preparatory measures including updating mobile numbers for OTP receipt, training staff on new authentication procedures, reviewing aggregate turnover calculations, and aligning operations with updated reconciliation requirements.

Challenges and Considerations

While the reforms promise significant benefits, businesses face implementation challenges. Small enterprises entering the e-invoicing framework must invest in compatible software and employee training. The mandatory ISD registration requires system updates, vendor communication, and additional compliance burden through separate return filing.

The 30-day e-invoice reporting deadline may initially strain businesses accustomed to flexible timing, potentially resulting in ITC loss for non-compliance. However, these measures aim to enhance tax transparency and reduce system leakages.

Future Outlook and Broader Implications

The GST reforms represent India’s commitment to creating a world-class indirect tax system that balances revenue requirements with ease of doing business. The move towards digitization, enhanced security, and simplified rate structure positions India’s tax framework among the most advanced globally.

These changes are expected to boost exports competitiveness by reducing input costs and stimulate domestic consumption through lower prices on everyday goods. The reforms also support the government’s Atmanirbhar Bharat vision by creating a more conducive business environment for domestic manufacturing and services.

The success of GST 2.0 will largely depend on smooth implementation, stakeholder cooperation, and continuous system refinements. Early indicators suggest strong government commitment to addressing implementation challenges through stakeholder consultations and phased rollouts.

As India approaches the Diwali 2025 implementation deadline, businesses and consumers alike can anticipate a more simplified, secure, and efficient tax ecosystem that reduces compliance burden while maintaining robust revenue collection mechanisms. These reforms mark a new chapter in India’s indirect tax evolution, promising to deliver tangible benefits across economic sectors while strengthening the foundation for sustained growth.

The Indian government’s thinking behind the proposed removal of the 28% and 12% GST rate slabs is driven by a clear objective to simplify the GST structure, enhance ease of doing business, and make goods and services more affordable for consumers.

Key Government Thinking and Rationale Behind Removing 28% and 12% GST Slabs:

- Simplification and Rationalization of GST Rates

- The government aims to reduce complexity by consolidating multiple GST rates into fewer slabs, improving the tax system’s transparency and efficiency.

- Removing the 28% and 12% slabs is part of moving towards a simpler two-tier GST system, primarily with 5% and 18% rates, thereby making tax computation and compliance easier for businesses.

- Reducing the Burden on Consumers

- The 28% slab primarily taxes luxury and sin goods, while the 12% slab covers many everyday goods.

- By moving most items from 12% down to 5% and majority of 28% slab items down to 18%, the government reduces the effective tax burden for consumers, boosting purchasing power and stimulating demand.

- Boosting Economic Growth and Consumption

- Lower GST rates on essential and common goods encourage higher consumption, which is critical for accelerating economic recovery and growth.

- The government expects these rate rationalizations to lead to increased disposable incomes and greater market expansion.

- Enhancing Compliance and Revenue Stability

- Fewer slabs reduce disputes and classification issues among taxpayers and tax authorities, leading to better compliance.

- Despite rate cuts, the government anticipates broadening the tax base and compliance to maintain or even increase revenue collection in the long run.

- Facilitating Industrial Competitiveness

- Rationalizing rates makes Indian goods more competitive domestically and internationally by reducing the cascading effect of taxes and lowering the cost of inputs.

- This is aligned with India’s vision to boost manufacturing under initiatives like “Make in India.”

- Stakeholder Consultations and Evidence-Based Policy

- The government conducted extensive consultations with industry, tax experts, and state governments to assess the impact before proposing changes.

- The decision reflects a balanced approach between fiscal prudence and promoting economic welfare.

- Strategic Timing with Political Will

- Announced as part of PM Modi’s Independence Day speech and scheduled for rollout by Diwali 2025, the changes symbolize transformative tax reform spearheaded by strong political leadership.

In summary, the removal of the 28% and 12% GST slabs reflects the government’s strategic move to create a simpler, more consumer-friendly tax structure that supports economic expansion, compliance efficiency, and sustained fiscal health while signaling India’s commitment to modernizing its indirect tax regime.